Table of Contents

Introduction: A Collision of Worlds

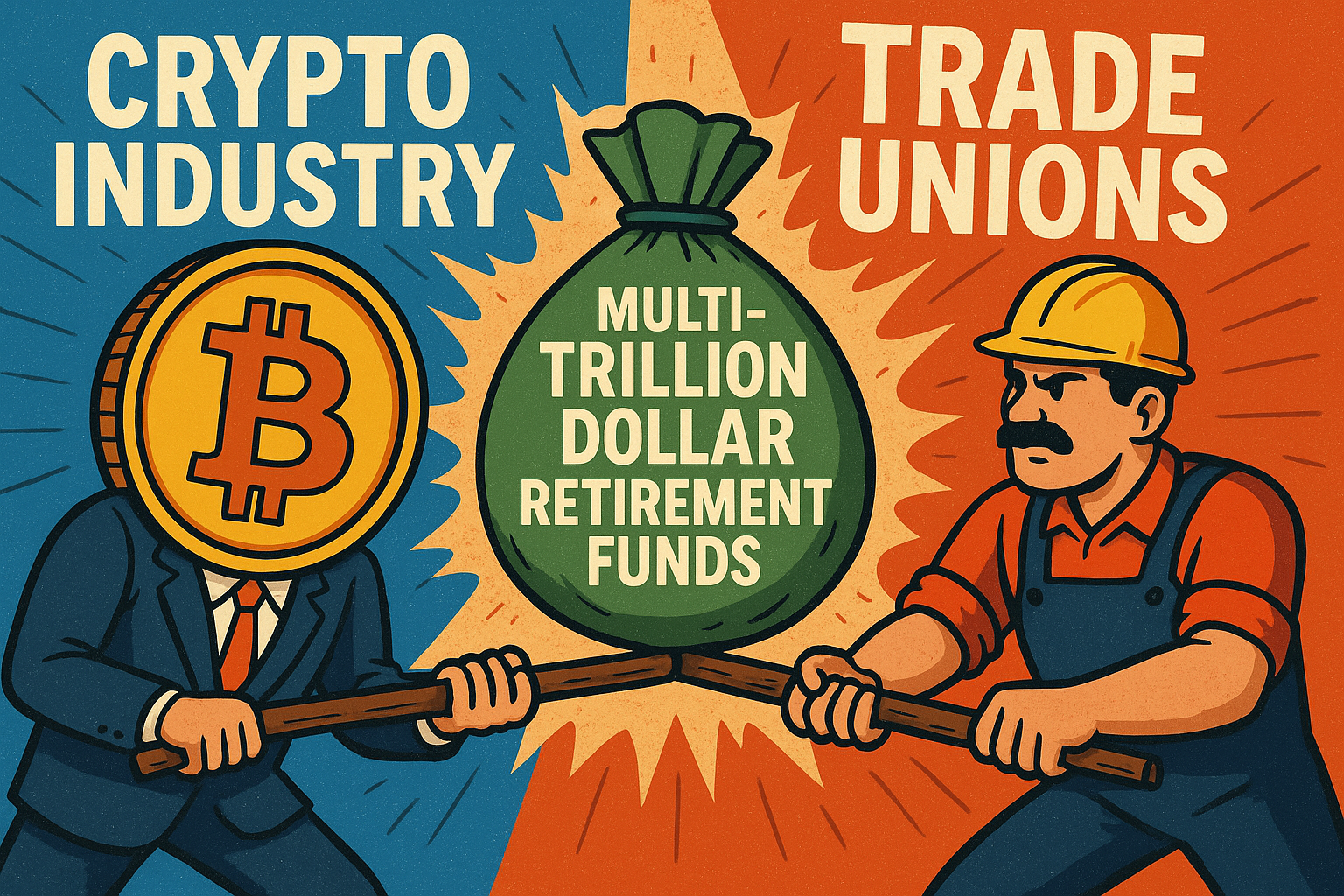

The financial world is undergoing a seismic transformation, and at the epicenter lies a nascent but assertive player—cryptocurrency. As blockchain adoption gains momentum and digital assets move steadily from fringe to mainstream, traditional institutions are grappling with how to respond. One of the most significant tensions emerging is between the crypto industry and trade unions—specifically surrounding the future of retirement and pension funds. On one side, cryptocurrency advocates see a massive, untapped opportunity: trillions of dollars in retirement capital currently tethered to slow-moving traditional assets. On the other, trade unions and regulatory bodies are holding firm against integrating digital assets, raising alarms about volatility, scams, and insufficient investor protections.

Yet, beneath the polarizing rhetoric lies a deeper truth—this confrontation isn’t merely a matter of economic theory or political ideology. It’s a pivotal moment that could reshape global wealth distribution, redefine the concept of financial security, and permanently alter how pension funds operate in the 21st century. Rather than resisting change, both the crypto world and traditional labor institutions have a rare chance to reimagine retirement investing in a way that balances growth, innovation, and protection for working-class savers.

Current Scenario: Barriers and Bottlenecks

Despite the rising popularity of digital assets, most pension and retirement funds remain locked out of the crypto market. Regulatory frameworks dating back decades continue to dictate the investment strategies of public and private-sector pension plans. These outdated policies often categorize all cryptocurrencies as "high-risk" or "speculative" assets, alongside penny stocks and junk bonds. As such, fiduciaries overseeing pension funds are typically prohibited—or heavily discouraged—from allocating even a small percentage into crypto holdings, even those with large market caps and proven performance histories such as Bitcoin (BTC) or Ethereum.

This exclusion persists even as the financial case for diversification into digital assets becomes stronger. Bitcoin, widely regarded as "digital gold," has consistently outperformed equities and bonds over extended time horizons. Ethereum, the backbone of decentralized finance (DeFi), powers an entire ecosystem of smart contracts and protocols transforming lending, borrowing, and trading. Still, pension boards and trade unions argue that the inherent price volatility and lack of regulatory clarity represent a dangerous gamble with retirees' money.

Yet what this perspective overlooks is the broader economic risk of clinging to outdated allocation models. Many pension funds are overexposed to bonds yielding negative real returns or equities trading at historically high price-to-earnings ratios. In a world dominated by inflationary pressures and shrinking yield environments, the notion of “prudent investing” needs to evolve. Otherwise, retirement portfolios will struggle to meet projected obligations, burdening future generations or forcing reductions in promised benefits.

Potential Impact: Trillions Waiting in the Wings

The possibilities for crypto integration into retirement portfolios are nothing short of revolutionary. The global retirement and pension management industry holds over $50 trillion in assets. If even a conservative estimate—say, 1%—of these funds were to be redirected into digital assets, the inflows would total around $500 billion. This type of capital injection could dramatically alter the structure and behavior of crypto markets, enhancing stability, liquidity, and legitimacy.

Institutional money not only brings capital; it brings discipline, risk oversight, and long-term investment horizons. The presence of these investors can act as a stabilizing force, reducing the extreme volatility often fueled by retail speculators and short-term traders. Moreover, seeing public pensions allocate even a fraction of their portfolios to cryptocurrency would send strong signals of acceptance to other market participants, potentially opening the floodgates for mass institutional adoption.

The next Bitcoin bull market or crypto boom might not be triggered by retail enthusiasm or new DeFi products—it could come from the strategic reallocation of pension capital. This shift could also democratize wealth creation, allowing everyday workers—not just tech-savvy investors or venture capitalists—to benefit from the rise of blockchain-based assets. If orchestrated correctly, retirement exposure to cryptocurrencies could become a powerful tool for income inequality mitigation and intergenerational wealth preservation.

Recommendations: A Path Forward

For crypto to be integrated into retirement funds meaningfully and responsibly, both policy and perception need to change. First, regulatory frameworks must be updated to distinguish between speculative tokens and established assets backed by solid fundamentals, large user bases, and substantial developer communities. Treating all cryptocurrencies the same is both inaccurate and counterproductive. Policymakers must create clear distinctions that allow approved digital assets to be incorporated into pension allocations under proper oversight.

Second, investment managers and unions should explore diversified crypto exposure through regulated vehicles. Cryptocurrency index funds, spot Bitcoin ETFs (where approved), crypto IRAs, and blockchain-focused exchange-traded products provide compliant avenues for accessing the market with reduced risk. Further, employing institutional-grade custody solutions—such as those offered by Coinbase Custody or Fidelity Digital Assets—can alleviate concerns about private key management, hacks, or scams.

Innovative models also deserve consideration. Tokenized pension funds could allow for real-time auditing, transparent fund governance, and even DAO-based management structures, where union members collectively vote on fund allocations using blockchain technology. Regulated platforms focusing on Staking-as-a-Service (SaaS) could offer consistent yield generation, similar to dividend-paying stocks or bonds, but with enhanced flexibility and digital efficiency. These structures can be crafted with built-in safeguards, balancing exposure with capital preservation.

Perhaps most importantly, labor leaders need to engage with crypto builders—not as opponents but as collaborators. Working with regulatory-compliant platforms and developers enables unions to shape the future of retirement in alignment with their values. Crypto is not just for the tech elite; it is a paradigm shift in finance, and its full potential can only be reached through inclusive dialogue, education, and common-ground policy reform.

Conclusion: Collaboration Over Confrontation

The standoff between trade unions and the cryptocurrency ecosystem is not an unresolvable impasse, but rather a reflection of the broader evolution unfolding in global finance. While the fears of volatility, scams, and systemic risk are not unfounded, the outright dismissal of blockchain investment opportunities under the guise of caution is a missed opportunity.

By engaging openly and reexamining their principles of fiduciary responsibility, unions can become powerful advocates for a more progressive and inclusive financial future. Embracing select digital assets under due diligence processes, utilizing institutional tools, and exploring new governance models like DAOs can allow retirement systems to innovate without sacrificing security. After all, the ultimate goal remains the same—providing stable, growing, and secure futures for workers and retirees. In that respect, the technological revolution offered by blockchain is not a threat. It’s a tool—one that requires collaboration, not confrontation, to unlock its full potential.

As the lines continue to blur between traditional finance and decentralized innovation, those prepared to adapt and explore this hybrid vision of wealth management will be best positioned. Pension funds don't have to choose between safety and growth—they can pursue both, guided by forward-thinking policies and a willingness to evolve. Forty years from now, we may look back on 2024 not as the year of conflict, but as the year that unions and crypto advocates found common ground—and transformed retirement finance forever.

{kind=link}